Unexpected medical bills can be overwhelming, but the No Surprises Act , effective since January 1, 2022, protects patients from surprise charges for out-of-network care in emergencies and certain non-emergency services. Here’s what you need to know:

- Key Protections: Patients pay in-network costs for emergency services, air ambulance services, and specific out-of-network care at in-network facilities.

- Good Faith Estimates: Uninsured patients must receive a cost estimate for scheduled services. If the final bill exceeds this estimate by $400 or more, they can dispute it.

- Dispute Resolution: Providers and insurers resolve payment disagreements through arbitration, shielding patients from involvement.

- Illinois-Specific Protections: Illinois has expanded federal protections, covering more provider types and services. Starting 2027, ambulance services will also be included.

These measures reduce financial stress, ensuring patients aren’t burdened by unexpected medical costs. If you’re in Illinois, understanding these rights can help you avoid surprise bills and manage healthcare expenses effectively.

How the No Surprises Act Protects Illinois Patients from Unexpected Medical Bills

No More Surprise Medical Bills: 5 Things To Know about the No Surprises Act Taking Effect in 2022

How the No Surprises Act Works

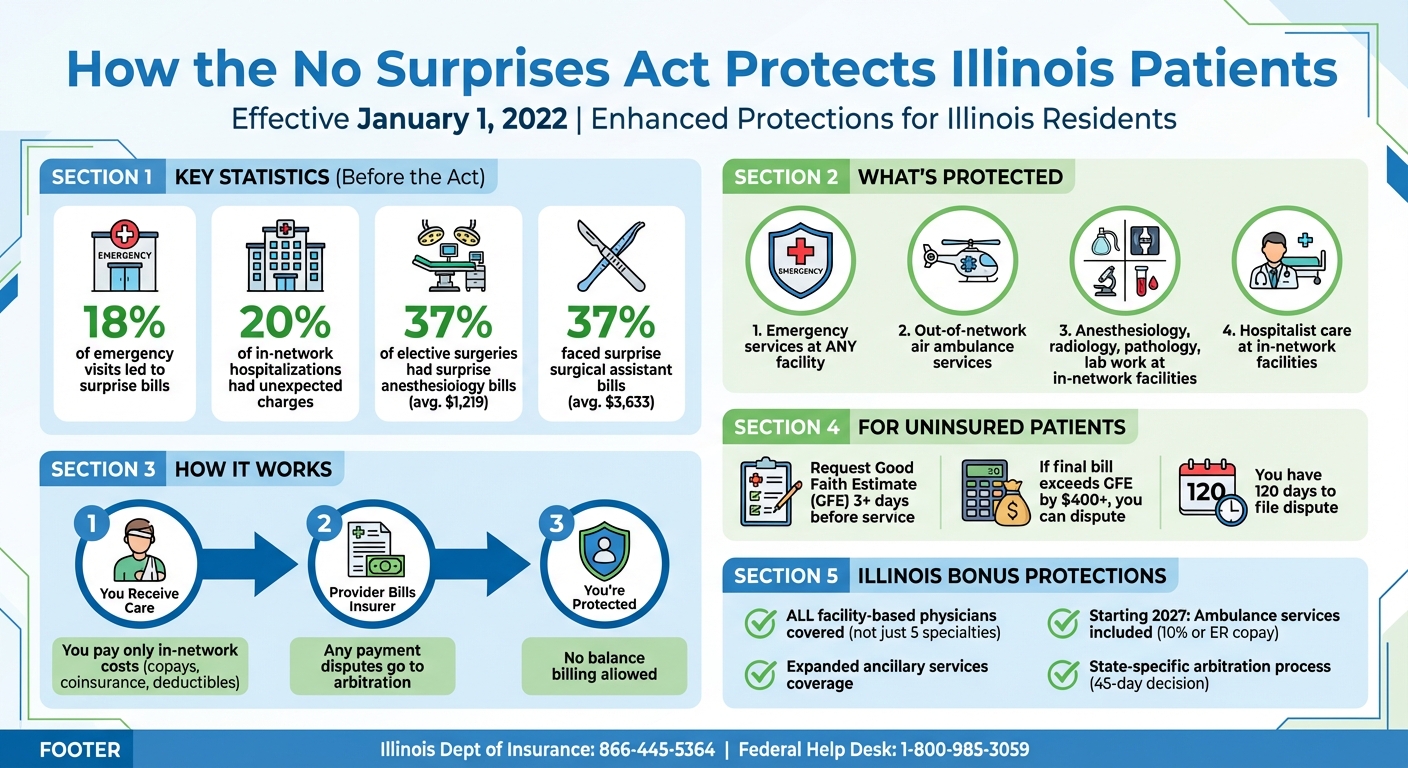

The No Surprises Act limits unexpected medical bills by prohibiting balance billing for out-of-network care, transferring payment disputes to providers and insurers instead. For patients, this means your costs are capped at the same level as in-network care. You’ll only be responsible for your usual copayments, coinsurance, and deductibles – even if treated by an out-of-network provider in certain covered situations. These protections apply to emergency services at any facility, out-of-network air ambulance services, and additional services like anesthesiology, radiology, pathology, lab work, and hospitalist care performed at in-network facilities.

Independent Dispute Resolution (IDR) Process

When providers and insurers disagree on payment for out-of-network services, they must first go through a 30-day open negotiation period to try to settle voluntarily. If no agreement is reached, either party can start the federal IDR process. This involves a certified arbitrator who reviews both sides’ final payment offers and chooses one. This "baseball-style" arbitration ensures a binding decision. For patients without insurance or those choosing not to use it, the Act offers extra protections through good-faith estimates.

Good-Faith Estimates for Uninsured Patients

Patients without insurance – or those not using it – are entitled to a written good faith estimate (GFE) of expected costs for non-emergency services scheduled at least three business days in advance. The GFE should detail the total expected cost of the primary service and any related expenses, such as tests, hospital fees, and supplies.

"You have the right to receive a Good Faith Estimate for the total expected cost of any non-emergency items or services. This includes related costs like medical tests and hospital fees." – UI Health

If your final bill is $400 or more above the GFE, you can dispute the charges. You have 120 calendar days from receiving the bill to start the dispute process. Be sure to keep a copy of your GFE as proof if your final bill exceeds the estimate by $400 or more.

Illinois-Specific Implementation of the No Surprises Act

Illinois has expanded upon the federal No Surprises Act by introducing additional protections and a distinct dispute resolution process tailored to the state’s needs.

Additional Protections in Illinois

Illinois has gone beyond the federal requirements by including broader protections for patients. The state now ensures coverage for all non-participating facility-based physicians, not just the five specialties previously regulated. This change significantly increases the scope of protection against surprise medical bills. Additionally, ancillary services – such as radiology, laboratory, anesthesiology, pathology, neonatology, assistant surgeons, hospitalists, and intensivists – are also covered. Cost-sharing for these services is capped at the lesser of the provider’s billed amount or the federal qualifying payment amount (QPA).

Starting January 1, 2027, Illinois will also extend protections to ambulance services, including both emergency and urgent situations. Patients will only be responsible for their in-network emergency room copayment or 10% of the recognized amount, ensuring more predictable costs for these critical services.

Revised Dispute Resolution Process in Illinois

Illinois has established its own process for resolving payment disputes, distinct from the federal framework. After a mandatory 30-day negotiation period, either party can request binding arbitration through the Illinois Department of Insurance . The arbitrator is required to deliver a decision within 45 days of the filing, providing a timely resolution.

If both parties cannot agree on an arbitrator, the Department of Insurance supplies a list of five candidates. Each side can veto two, leaving the remaining individual to serve as the arbitrator. Importantly, Illinois law ensures that arbitrators do not default to using the qualifying payment amount as the sole determinant for what is owed. As outlined in Public Act 104-0248:

"The arbitrator shall not establish a rebuttable presumption that the qualifying payment amount should be the total amount owed to the provider or facility by the combination of the issuer and the insured, beneficiary, or enrollee."

This ensures that arbitrators weigh multiple factors when deciding on fair payment, rather than relying exclusively on the insurer’s benchmark rate. These additional state-level measures bolster the federal protections, offering Illinois residents greater safeguards against unexpected medical expenses.

sbb-itb-a729c26

Impact on Illinois Residents

Lower Out-of-Pocket Costs for Patients

The No Surprises Act has brought much-needed financial relief to residents in Illinois. Before this legislation, surprise medical bills were alarmingly common – 18% of emergency visits and 20% of in-network hospitalizations led to unexpected charges. Certain specialties were particularly problematic. For instance, 37% of patients undergoing elective surgeries faced surprise bills for anesthesiology services, averaging $1,219. Similarly, 37% of patients billed for surgical assistant services encountered charges averaging $3,633.

Thanks to the act, Illinoisans now pay only in-network cost-sharing amounts for specific services like emergency care, radiology, pathology, and anesthesiology. These costs count toward their in-network deductibles and annual out-of-pocket maximums, helping prevent financial strain. For uninsured patients, the law includes protections as well – if a bill exceeds their good faith estimate by more than $400, they can dispute the charge. To safeguard themselves, patients are encouraged to request a written estimate at least three business days before scheduled services and retain all related documents for potential disputes.

These measures not only ease the financial burden on patients but also influence how healthcare providers and insurers operate.

Effects on Healthcare Providers and Insurers

Healthcare providers and insurers have had to adapt significantly since the act took effect. Emergency departments and urgent care centers now face the challenge of implementing new billing systems while ensuring they clearly communicate network affiliations to patients – a change that adds layers of administrative work. As CBIZ explains, "The NSA ensures that patients requiring emergency medical attention are charged in-network rates regardless of the service provider’s network status. This eliminates the fear of financial distress… but presents operational challenges for emergency centers".

Under the new system, providers must directly negotiate reimbursements with insurers or turn to the Independent Dispute Resolution (IDR) process, creating additional administrative hurdles for both sides. A study from 2025 highlighted that similar protections in other states have successfully reduced patient costs. However, compliance issues remain. By June 2022 – just six months after the act’s implementation – 20% of American adults who should have been protected still reported receiving surprise bills, signaling that more work is needed to ensure full compliance.

While these operational changes introduce complexities for healthcare entities, they aim to prioritize patient affordability and establish fair payment practices across the system.

How Health Insurance Brokers Support Illinois Residents

Personalized Insurance Solutions

Health insurance brokers play a key role in helping Illinois residents navigate their options under the No Surprises Act. For instance, Illinois Health Agents provides free consultations to compare private insurance plans and Marketplace (ACA) options. This ensures individuals can find in-network coverage tailored to their specific needs.

With upcoming market shifts in 2026, such as the departure of insurers like Aetna CVS Health and Health Alliance , brokers help residents select plans that account for protected out-of-network services, applying them toward in-network deductibles and out-of-pocket maximums. They also advise uninsured individuals to request written cost estimates and keep documentation in case disputes arise.

Beyond plan selection, brokers simplify the complexities of these protections, making them easier to understand and use.

Guidance on No Surprises Act Protections

Another critical service brokers provide is educating residents about the No Surprises Act. They explain the differences between in-network and out-of-network charges and stress that balance billing is prohibited for emergency care and certain non-emergency services. This insight is especially helpful when residents encounter "Notice and Consent" forms. As Mayo Clinic emphasizes:

"You are never required to give up your protections from balance billing. You also are not required to get out-of-network care." – Mayo Clinic

Brokers encourage clients to thoroughly review these forms, reminding them that they can refuse to sign if it compromises their protections.

Additionally, brokers clarify continuity of care provisions. For example, patients with serious or chronic conditions can continue receiving in-network rates for up to 90 days if their provider leaves the network. They also connect clients with resources like the Federal No Surprises Helpdesk (1-800-985-3059) or the Illinois Department of Insurance (877-527-9431) for further assistance and enforcement.

Conclusion

The No Surprises Act offers patients protection from being caught in direct billing disputes between healthcare providers and insurers. Since January 1, 2022, emergency services and specific non-emergency care at in-network facilities can no longer result in surprise medical bills. Insured patients are charged in-network rates for out-of-network emergencies, while uninsured patients receive clear cost estimates and can dispute bills that exceed those estimates by more than $400. These federal measures provide a solid baseline of protection, which Illinois has further strengthened with its state laws.

Illinois has taken these protections a step further. State law now bans all facility-based physicians at in-network hospitals from balance billing patients. Together, these federal and state measures create a robust safety net for Illinois residents, shielding them from unexpected medical costs.

Understanding these protections can be challenging, which is why expert advice is invaluable. Health insurance brokers, like Illinois Health Agents, can help you understand your rights and assist in resolving billing disputes. Whether you’re navigating changes in the insurance market, choosing a new plan, or addressing a surprise bill, professional guidance ensures you’re making well-informed decisions.

If you encounter a bill that violates these protections, contact the Illinois Department of Insurance at 866-445-5364 or the federal No Surprises Help Desk at 1-800-985-3059. Be sure to keep all relevant documents, such as Good Faith Estimates and Explanation of Benefits statements, as they can serve as crucial evidence in resolving disputes.

These layers of protection work together to ensure you won’t bear the burden of unexpected billing issues.

FAQs

How does the No Surprises Act protect Illinois residents differently from federal protections?

The No Surprises Act protects Illinois residents by banning balance billingfor services from out-of-network healthcare providers at in-network hospitals or facilities. This means patients won’t face unexpected medical bills when seeking emergency care or receiving treatment at in-network locations.

Illinois has also aligned with federal guidelines by adopting the definition of a qualifying payment amount– the benchmark used to establish fair reimbursement rates for out-of-network providers. On top of that, healthcare providers in the state must give good faith estimatesfor scheduled services, ensuring that patients have a clearer understanding of potential costs.

Together, these steps aim to minimize financial surprises for patients while promoting fairness among patients, providers, and insurers.

What should I do if my medical bill is more than $400 higher than my Good Faith Estimate?

If your medical bill exceeds your Good Faith Estimateby more than $400, the first step is to request an itemized bill from your healthcare provider. Carefully review the charges and compare them with the original estimate to spot any discrepancies. If something doesn’t add up, reach out to your provider or insurance company to dispute the charge. Thanks to the No Surprises Act, you’re protected in these cases. You also have the option to file a complaint or pursue resolution through the designated channels. Address the issue promptly to make sure your rights are protected.

What is the process for resolving out-of-network billing disputes in Illinois?

The federal No Surprises Actprovides Illinois residents with protection against unexpected out-of-network medical bills. When disputes arise between healthcare providers and insurance companies over payments, they can turn to the Independent Dispute Resolution (IDR)process. This system uses a certified third-party arbitrator to review the case and make a binding decision. The arbitrator considers various factors, such as median in-network rates for similar services, to ensure a fair outcome.

In Illinois, both state and federal authorities share the responsibility of enforcing these protections. The IDR process plays a key role in resolving payment disagreements, shielding patients from surprise costs while promoting transparency in medical billing practices.