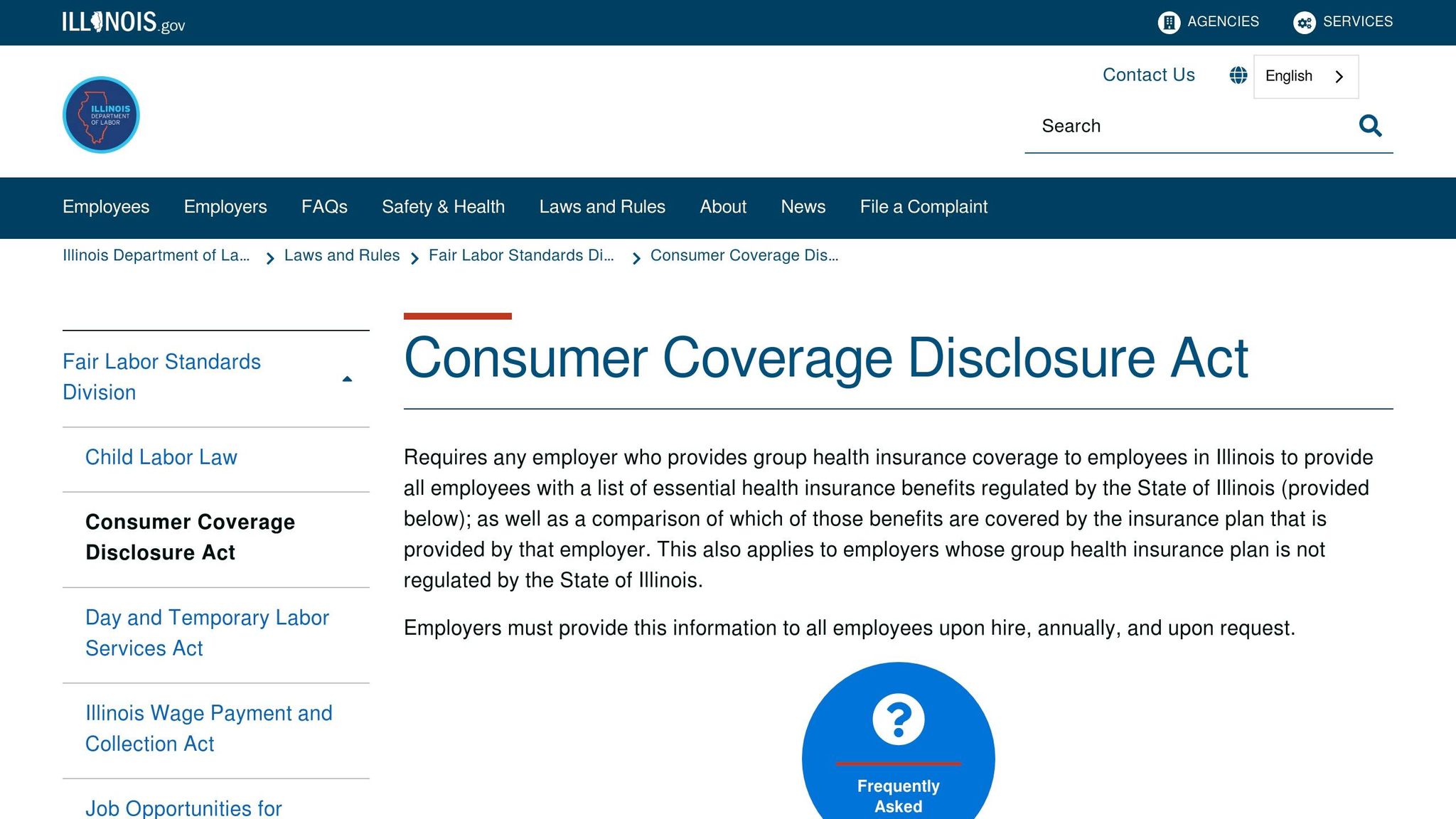

Employers in Illinois must comply with the Consumer Coverage Disclosure Act (CCDA), which has been in effect since August 27, 2021. This law requires them to provide employees with a written comparison of their group health insurance plan against the state’s Essential Health Benefits (EHBs). The goal is to help employees understand their coverage and compare it to plans available through Get Covered Illinois .

Key Takeaways:

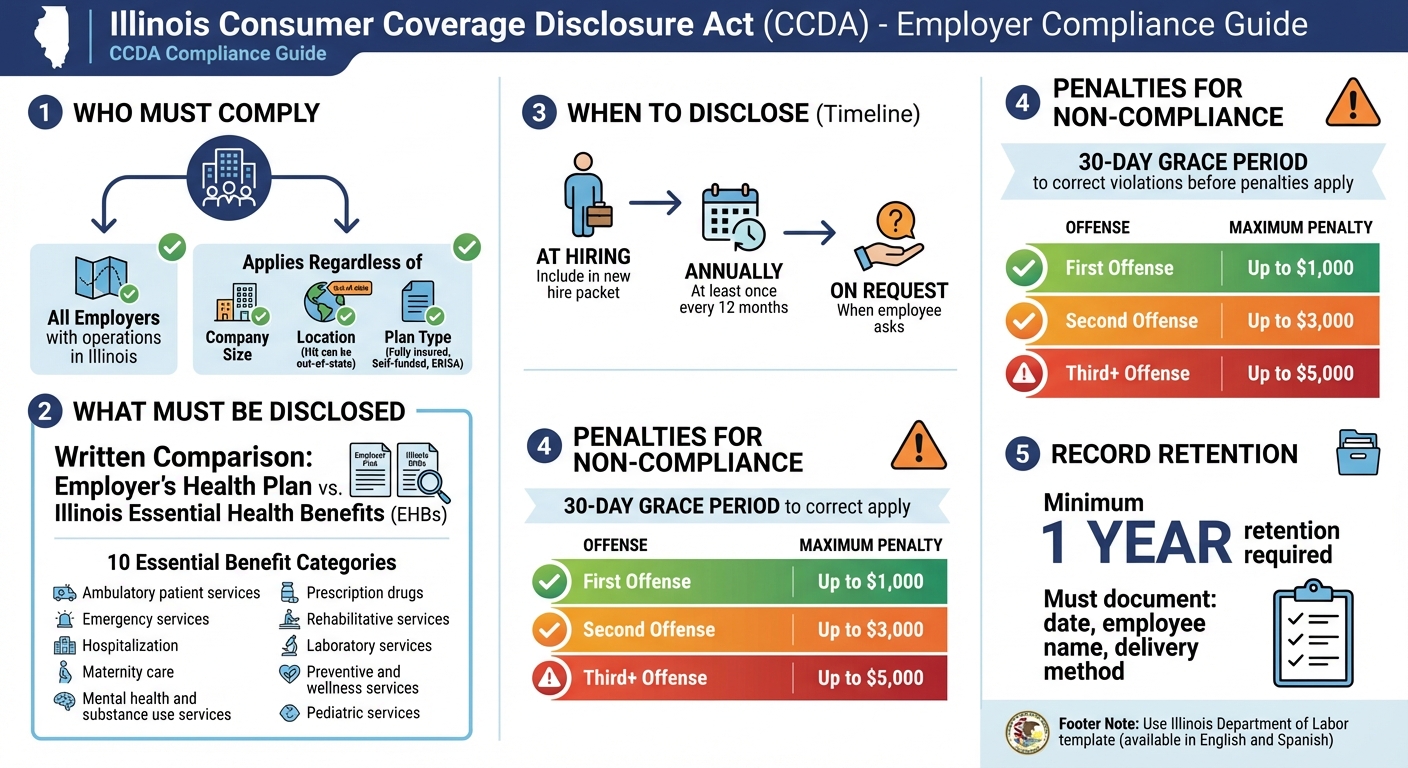

- Who Must Comply?All employers with operations in Illinois, regardless of size or location, offering fully insured or self-funded plans.

- What Must Be Disclosed?A written comparison of the employer’s health plan to Illinois’ EHBs in 10 categories (e.g., hospitalization, maternity care, prescription drugs).

- When to Disclose?

- At hiring

- Annually (at least once every 12 months)

- Upon employee request

- Penalties for Non-Compliance:Fines range from $500 to $5,000 per offense, depending on the violation and business size.

- Record Retention:Employers must retain disclosure records for at least one year.

Employers can use the Illinois Department of Labor ‘s templatefor disclosures and should work with insurers or brokers to ensure accuracy. Proper compliance not only avoids penalties but also helps employees make informed decisions about their healthcare options.

Illinois CCDA Compliance Requirements and Penalties for Employers

Understanding the Consumer Coverage Disclosure Act

What the Act Aims to Accomplish

The Consumer Coverage Disclosure Act (CCDA) is designed to give employees greater clarity about their health benefits. It requires employers to provide a written comparison of their group health insurance benefits against the essential health benefits (EHBs)offered through Get Covered Illinois, the state’s health insurance marketplace. However, this doesn’t mean employers have to match every benefit. As the Illinois Department of Labor clarifies:

The Consumer Coverage Disclosure Act does not impose coverage requirements on employers. It only imposes disclosure requirements.

This transparency helps employees see what their employer’s plan covers – and what it doesn’t – so they can decide if their current coverage meets their needs or if a marketplace plan might be a better fit.

The comparison focuses on 10 essential benefit categories, including:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Maternity care

- Mental health and substance use services

- Prescription drugs

- Rehabilitative services

- Laboratory services

- Preventive and wellness services

- Pediatric services

If a plan only partially meets a requirement – for example, covering three months of cardiac rehab when six months is the benchmark – it should be marked as "Partially" covered, with a brief explanation provided.

Next, let’s look at which employers and plans are required to comply with the Act.

Which Employers and Plans Must Comply

The disclosure rule applies to employers offering any type of health plan, whether it’s fully insured, self-funded, or governed by ERISA. To determine if the Act applies, the Illinois Department of Labor uses a "base of operations" test. For example:

- An employee working at an Illinois store for a company based in Missouri would be covered.

- An employee with an Illinois office who travels to other states for deliveries would also fall under the Act.

- Remote workers living in Illinois could be included, depending on their work arrangement.

Employers with out-of-state or remote employees should carefully review each situation to ensure they meet the Act’s requirements.

sbb-itb-a729c26

What Employers Must Disclose

Comparing Plans to Essential Health Benefits

Employers are required to create a written comparison that evaluates how their group health plan stacks up against Illinois’ Access to Care and Treatment Benchmark Plan and the Pediatric Dental Plan. This involves examining each of the 10 essential health benefit categories and marking whether the plan provides full, partial, or no coverage for each.

For instance, if a plan offers cardiac rehab for 3 months instead of the required 6 months, it should be labeled as "Partially" covered, along with a brief explanation. The Illinois Department of Labor emphasizes accuracy in these evaluations:

"Answering ‘yes’ if the coverage does not match the full extent of the benchmark plan may be considered misinformation." – Illinois Department of Labor

To ensure compliance, employers should work closely with their insurer or broker. Illinois Health Agents can also assist in verifying that comparisons align with benchmark standards.

When and How to Provide Disclosures

Once the plan comparison is prepared, employers must ensure timely and clear delivery of disclosures. The Consumer Coverage Disclosure Act specifies three key times when disclosures must be provided: during an employee’s initial hiring process, at least once every 12 months, and upon an employee’s request.

Disclosures can be distributed in various formats, such as email, through internal company websites, or as physical copies. Incorporating these disclosures into existing processes – like new hire onboarding packets or annual open enrollment materials – can simplify compliance and maintain consistency.

Record Retention Requirements

Accurate record-keeping is another critical requirement. Employers need to retain documentation of all disclosures for at least one year. This includes maintaining records of when each disclosure was provided, the recipient, and the delivery method. For example, a log or digital record listing the date, employee name, and how the disclosure was delivered (e.g., email or hard copy) should be kept. Make sure all documentation remains accessible for a minimum of one year.

New Illinois State Law Imposes Disclosure Requirements on Group Health Plans

Tools to Help Employers Meet Requirements

Employers can simplify the process of meeting CCDA requirements by using specialized tools and seeking expert assistance.

Using the Illinois Department of Labor Template

The Illinois Department of Labor (IDOL) offers a model disclosure template in both Excel and PDF formats. This template is designed to help employers compare their health plans to the state’s Essential Health Benefits (EHBs). It provides a detailed list of benefits alongside their corresponding Benchmark Page # Reference, making it easier to ensure compliance with state standards.

Although using the IDOL template is optional, it offers a clear structure to ensure all necessary elements are addressed. The department regularly updates the template – recent versions were released for both 2024 and 2025 to reflect the latest standards. To stay current, employers should download the updated template each year to align with any changes in benchmark requirements.

For workplaces with diverse teams, a Spanish-language version of the template is also available. To ensure proper formatting when printing, use the "Set Print Area" function in the Excel Page Layout tab.

While the template is a helpful tool, professional guidance can add an extra layer of accuracy.

Getting Help from Insurers and Brokers

Insurance providers, brokers, or Third-Party Administrators (TPAs) are valuable resources for employers navigating CCDA compliance. They can supply comprehensive policy documents and assist in aligning your coverage with the state’s EHB list.

Additionally, Illinois Health Agents can help verify that your plan meets benchmark standards and address any gaps in coverage. Using these resources not only ensures compliance but also demonstrates a commitment to providing clear and accurate disclosures to employees.

For further assistance, employers can contact the IDOL Compliance Unit at 312-793-2800 or email [email protected] .

Penalties for Failing to Comply

The Illinois Department of Labor (IDOL) is responsible for enforcing the Consumer Coverage Disclosure Act and may perform inspections to ensure businesses are following the rules. If a violation is found, employers are given a 30-day grace period through a notice to correct the issue before any financial penalties are applied. During this time, businesses must distribute the required disclosures to avoid fines. If the issue isn’t resolved within the grace period, penalties start to escalate.

Civil penalties can range from $500 to $5,000 per offense. The exact fine depends on factors like the size of the business, the seriousness of the violation, and whether the employer made genuine attempts to comply. Here’s a breakdown of the maximum penalties:

| Offense Number | Maximum Penalty |

|---|---|

| First Offense | Up to $1,000 |

| Second Offense | Up to $3,000 |

| Third or Subsequent Offense | Up to $5,000 |

Non-compliance carries risks beyond just fines. Employers may face administrative hearings if employees file complaints. If fines remain unpaid, the IDOL can escalate matters by filing a civil lawsuit in circuit court. Additionally, employers are required to keep records showing that each eligible employee received the disclosure, and these records must be retained for at least one year. Failing to provide these records during an inspection is considered a violation.

There’s also a potential for misunderstandings. If the disclosures indicate "No" or "Partially" covered benefits, employees might incorrectly assume their employer is offering inadequate or illegal coverage, even if the plan complies with legal standards. This kind of confusion can damage trust and lead to unnecessary tension in the workplace. Staying compliant not only helps avoid penalties but also ensures transparency and fosters trust with employees.

How Employers Can Stay Compliant

Setting Up a Disclosure System

To maintain compliance, employers need a well-organized disclosure system that keeps employees informed about their health coverage. This system should address three key moments: hiring, annual open enrollment, and when an employee requests information. Including the CCDA disclosure in both new hire packets and open enrollment materials ensures employees have the details they need. As Stephen J. Evans, Partner at BCLP , explains:

In practice, an employer should include the CCDA disclosure as part of a new hire packet for employees or otherwise provide it at the time of hire.

To ensure your plan aligns with Illinois Essential Health Benefits, collaborate with your insurance carrier, broker, or third-party administrator. Karen Breitnauer, Director of Employee Benefits Compliance at M3 Insurance , advises:

Employers should consult with their carriers or third?party administrators for assistance with the disclosure.

It’s also important to document each disclosure by recording the employee’s name, the date, and the delivery method. This helps meet the one-year retention requirement. Once your system is set, focus on how to communicate these disclosures effectively to your employees.

Communicating Disclosures to Employees

After setting up your disclosure system, ensure employees receive the information in formats they can easily access. Flexible delivery methods are key for compliance. Disclosures can be shared via email, provided as printed copies, or posted on a regularly used platform like a company intranet or benefits portal. An online benefits portal is particularly useful for centralizing all necessary information in one convenient location.

When completing the disclosure form, accuracy is critical. For example, if a benefit partially matches the benchmark (like offering three months of rehab instead of six), mark it as "Partial" and provide a brief explanation. This level of detail reduces confusion for employees and demonstrates your compliance efforts, which the IDOL considers when evaluating penalties.

For employers needing tailored advice on creating an effective disclosure system and ensuring clear communication, local resources like Illinois Health Agents can provide valuable support.

Conclusion

Illinois’ disclosure laws empower employees to compare their employer’s health plans with the state’s essential benefits. As Stephen J. Evans, Partner at BCLP, explains:

The intent of the CCDA is to help employees make informed decisions about whether the health insurance coverage offered to them via their employer best meets their needs.

This level of transparency ensures workers understand exactly what their coverage includes – and where it might fall short. For employers, this clarity is not just about meeting legal obligations; it’s a step toward building trust with their workforce.

Compliance with these laws applies to nearly all employers with staff in Illinois, regardless of company size or the type of insurance plan they offer. This includes self-funded plans and those governed by ERISA. Beyond avoiding penalties, providing clear and timely disclosures reflects a commitment to openness, which can strengthen employee confidence.

Fortunately, meeting these requirements doesn’t have to be overwhelming. Employers can simplify the process by using tools like the Illinois Department of Labor’s (IDOL) disclosure template. Collaborating with insurance carriers or brokers ensures accuracy, while integrating disclosures into hiring and benefits workflows keeps things organized. To protect both employees and the business, it’s essential to document each disclosure and retain records for at least one year.

For those seeking tailored support, Illinois Health Agents offers specialized guidance in group health insurance. They can help employers create a disclosure process that aligns with state standards while addressing employee needs effectively.

FAQs

Does the CCDA apply to my remote employees in Illinois?

Yes, the CCDA applies to remote employees in Illinois if they are authorized to work by your company. This law mandates that health plan disclosures be provided to all employees working in Illinois, no matter where they reside.

How is a benefit determined to be ‘Full,’ ‘Partial,’ or ‘No’ coverage?

A benefit is categorized as Full, Partial, or Nocoverage by evaluating how the employer’s health plan aligns with Illinois’ essential health benefits requirements. Fullcoverage indicates that all essential benefits are included, Partialmeans only some are provided, and Nosignifies none are offered. These classifications follow the disclosure rules established under Illinois law.

What records should we keep to prove we sent the CCDA disclosure?

Employers need to keep thorough records for at least one year to show they’re meeting CCDA disclosure requirements. These records should include copies of the written disclosures, proof of delivery(like email confirmations or posting logs), and any related correspondence.